Insight:

The recent depreciation of the RMB exchange rate is mainly driven by the strong US dollar and weak export expectations. Weaker export expectations are the direct cause of this exchange rate breakthrough. In fact, from the fourth quarter of last year, the US dollar index and the RMB exchange rate continued to be a bifurcated state, while the most fundamental factor underpinning the bifurcation was the strength of exports to the RMB exchange rate. At the same time, from the perspective of market sentiment, a break in this key point of 6.40 was accompanied by a catharsis of market sentiment.

Looking ahead, strong dollar and weak export expectations are difficult to change in the short term. Until US inflation data are available in April, the US Federal Reserve is expected to aggressively guide interest rate hikes until inflation is certain, so it is relatively certain that the RMB will come out of the lowest point, but the extent of the subsequent depreciation depends largely on the interpretation of the dollar index and China US fundamentals. Moreover, the most critical variable in whether the reversal of the China US interest rate differential will continue to lead to capital outflows is the covid-19 situation and the performance of the domestic economy. If there is an obvious inflection point in the epidemic and domestic confidence in stable growth changes, then capital outflows may come to an end. The pressure on the RMB exchange rate will be alleviated.

Main Content:

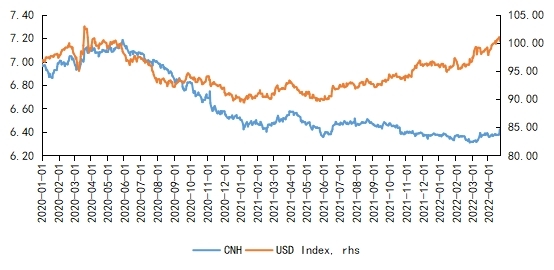

On April 20, 2022, both CNY and CNH broke through 6.40, hitting new highs since October 19, 2021. After half a year, the RMB rose to 6.40 again, and even broke its previous record. It coincides with the inversion of the interest rate gap between China and the United States, the domestic epidemic situation, and the failed expectation of an increase in money supply once again.

Figure 1: yesterday's CNH exchange rate was 6.40 (%)

Source: IFind Nanhua Research

In our view, the recent depreciation of the RMB exchange rate is mainly driven by the strong US dollar and weak export expectations, especially the weakened export expectation is the direct cause of this exchange rate breakthrough. In fact, from around the fourth quarter of last year, the US dollar index and the RMB exchange rate continued to be a bifurcated state, while the most fundamental factor underpinning the bifurcation was the strong export to the RMB exchange rate. At the same time, the key breakthrough of 6.40 was accompanied by a catharsis of market sentiment.

Figure 2: RMB exchange rate and dollar index split since the fourth quarter of last year

Source: Wind Nanhua Research

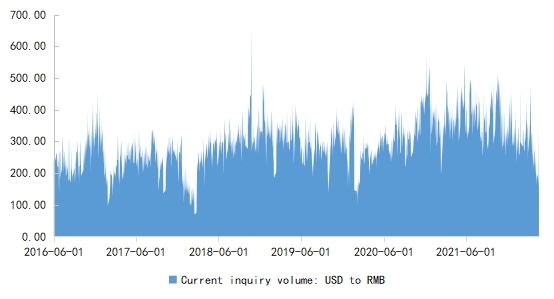

I.Market sentiment changed after key point breakthrough

First, from the index of transaction volume of CNY spot inquiry, after breaking through 6.40 and walking out of the market arc bottom on April 20, the transaction volume was obviously heavy. The RMB market sentiment, which had been sluggish due to the impact of the epidemic, had a clear catharsis. The transaction volume is at the historical quantile of 80.8%, a new high since March 15 this year, that is, a new high after the outbreak of this wave of epidemics.

Figure 3: USD/RMB spot inquiry transaction volume increased on 20 April

Source: IFind Nanhua Research

II.The weakening of export expectations has shaken the confidence in RMB

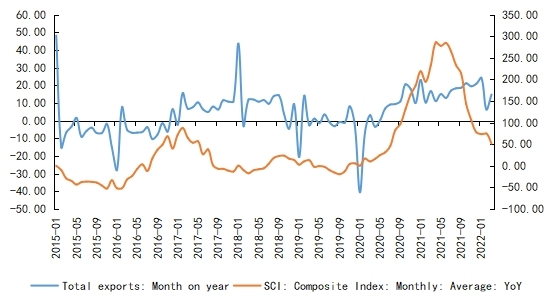

Second, the strong export expectation that supported the RMB's exchange rate was affected by the epidemic. The slowdown in export growth was within the market's benchmark expectation. However, the massive outbreak in Shanghai and Jilin since the end of March not only made it more difficult to achieve the domestic growth target, but also accelerated the expectation of a weaker export in the short term. It significantly undermined the previous strong RMB. This can be demonstrated from three perspective.

1) From the perspective of PMI's new export order index, which is a forward-looking indicator of exports, new export orders have been running below the confidence threshold since last May, showing that the real export volume is falling back. As of March, new export orders were 47.2%, at a historical quantile of 14.9%, which is significantly weaker.

2) From the point of coincident Indicator of exports, the BCI recruitment index is generally in line with the apparent export trend in recent years, as exports are mainly in labor intensive industries, so actual recruitment condition tends to represent the performance of actual export orders. Affected by the epidemic, people in the whole region or some regions are often required to undergo covid-19 testing due to the emergence of confirmed cases, and the flow of people and logistics is restricted. Combined with a marked increase in the unemployment rate of urban area in March, the weakening of the recruitment index in April is almost a definitive event, indicating a weakening of exports in April.

3) In terms of the performance of SCFI (weekly frequency), the April average year on year growth rate of the SCFI fell to the lowest since August 2020. High frequency data also show that the outbreak significantly weighed on exports in April.

Figure 4: strong exports since last year is the fundamental reason underpinning the divergence between the RMB exchange rate and the dollar index

Source: IFind Nanhua Research

Figure 5: SHANGHAI CONTAINERIZED FREIGHT INDEX (SCFI) heralds weaker exports in April

Source: IFind Nanhua Research

III.A strong dollar index and an inverted China-US interest rate differential are helping

The recent strength of the US dollar index at the 100 mark was largely driven by expectations of an increase in interest rates from the US Federal Reserve, as well as monetary policy posturing by the European Central Bank and the Bank of Japan, which contributed to the US dollar's recent strength. The US dollar index itself remained strong amid the more aggressive stance of the Fed's rate hike expectations in the first half of the year, but the recent rate hike is clearly more extreme. On April 19, the well-known ‘Eagle King' Brad of the Federal Open Market Committee of the Federal Reserve announced that he would not ‘rule out' the possibility of a 75-basis point increase, with interest rate hike expectations clearly becoming more aggressive. In relative terms, the ECB was decidedly dovish this month, and the sharp depreciation of the yen has significantly faded its safe-haven attributes, which in turn has made the already strong dollar index more favored by the market with the help of safe-haven attributes.

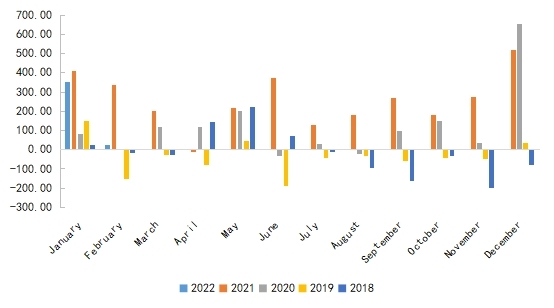

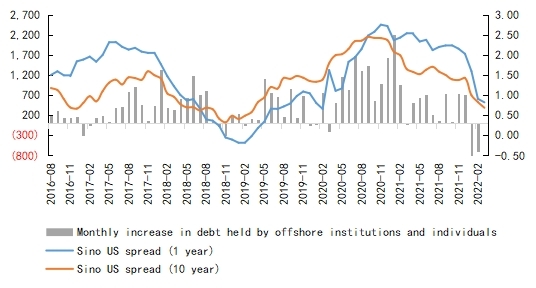

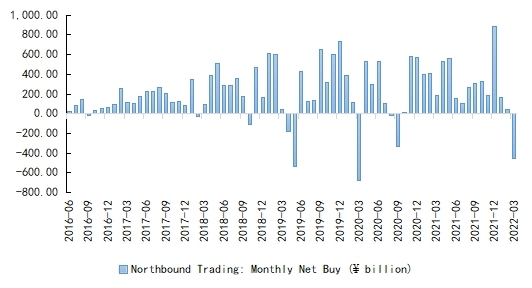

China US interest rate spreads have also been reversed recently, and foreign outflows have been more pronounced recently. In practice, China US interest rate spreads do not explain the RMB exchange rate well, and in some years, they have even been positively correlated, contrary to theory. But if there is a capital outflow after the spread is inverted, it will bring downward pressure from supply and demand as well as sentiment to the RMB exchange rate. In contrast to history, the stage of capital outflow usually corresponds to the depreciation of the RMB, including the recent outflow of funds from offshore institutions and personal debt, as well as the apparent outflow of funds from land stock and stock exchanges.

Figure 6: Outflows from offshore institutions and individual holdings

Source: IFind Nanhua Research

Figure 7: Net outflow of funds from LUJIAZUI Stock Connect in March

Source: IFind Nanhua Research

IV.Medium to short term RMB depreciation pressure is relatively limited

Now, strong dollar and weak export expectations are hard to change in the short term, and, until US inflation data are available in April, the US Federal Reserve is expected to aggressively guide interest rate hikes until inflation is certain, so the RMB leaving its lowest point is relatively certain, but the extent of the subsequent depreciation depends largely on how the dollar index compares with the US and China fundamentals. Moreover, the most critical variable in whether the reversal of the China US interest rate differential will continue to lead to capital outflows is the outbreak and the performance of the domestic economy. If there is a significant inflexion point in the outbreak and confidence in stable domestic growth changes, the outflow may end, and the pressure on the RMB exchange rate will ease.